Autumn Statement 2023: Confirmation of R&D Tax Credit Schemes Merger

During the announcement on 22nd November, Chancellor Jeremy Hunt confirmed the implementation of the merger of the two R&D tax credit schemes, a plan initially proposed in July 2023. From April 2024, the SME scheme for small to medium-sized enterprises and the RDEC scheme for larger businesses will be unified into a single, comprehensive scheme.

Representing one of the most significant changes to R&D tax relief in its history, large-scale changes were anticipated by many industry commentators following recent measures against non-compliance and increasing fraud instances, especially after the Spring Budget 2023, which significantly reduced the relief rates for claims under the SME schemes.

Why are the schemes being merged?

The extensive reforms in the R&D tax credit schemes, including their merger, were somewhat anticipated following the significant rate changes in the Spring Budget 2023. Many hoped these broad changes would delay further alterations like the merger for a year or two, however, this has not been the case.

Chancellor Jeremy Hunt highlighted potential government savings of £280 million due to the merger. However, the primary drivers for this move seem to be the increasing issues with non-compliance and the rising incidents of fraud in recent years. The statement emphasised ‘simplification’ as a key goal.

Despite the aim for simplification, the new structure introduces multiple rates of relief, which could be seen as contradictory to the simplification goal.

Key Announcements from the Statement:

R&D Tax Credit Scheme Merger:

- Effective from 1st April 2024, the SME and RDEC schemes will merge, affecting both profit-making and loss-making businesses not eligible for the ‘intensive’ scheme.

- The merger will primarily follow the outgoing RDEC rules with a headline rate of 20%. Profitable businesses will claim 16.2% or 15% relief based on their tax rate.

- Loss-making businesses will see a 19% tax rate, translating to a 16.2% relief rate, offering an increased benefit compared to the former RDEC scheme’s 25% tax rate.

Reduced SME R&D ‘Intensive’ Threshold:

- Announced in the Spring Budget 2023, the R&D ‘intensive’ scheme initially allowed SMEs with R&D expenses over 40% of their total expenditure to claim higher relief rates. This threshold is now reduced to 30% from April 2024, anticipated to permit over 5,000 more businesses to claim under the scheme.

- A one-year grace period will be available for businesses with fluctuating ‘R&D intensity’ levels below 30%, aiding those with variable R&D spending.

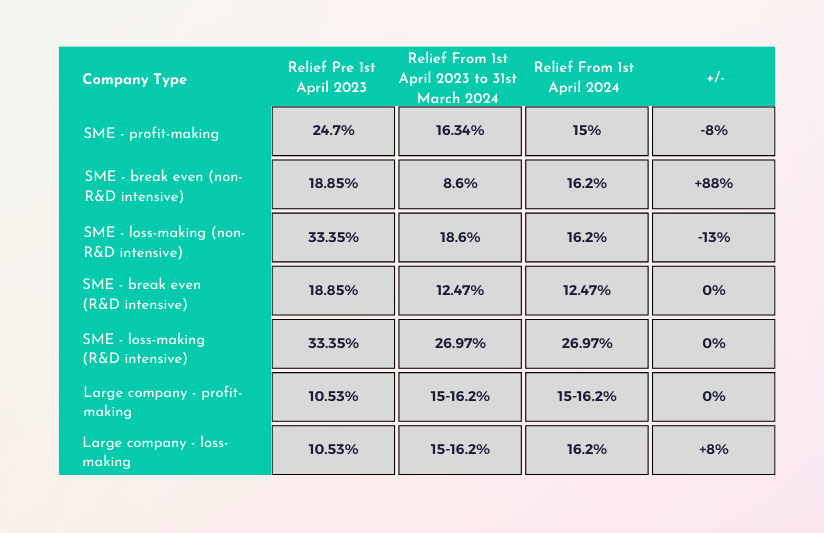

The new rates of relief

The contrasting outcomes from these changes reveal distinct winners and losers. Notably, loss-making SMEs that don’t qualify as ‘R&D intensive’ are likely to be the most adversely impacted by the merger of the schemes. While the adjustments to the R&D intensive scheme are generally seen as positive, the substantial reduction in relief rates for small, loss-making businesses — a 51% decrease from the rates prior to April 2023 to those post-April 2024 — is significant. These businesses, often unable to fund their R&D initiatives internally, are particularly susceptible to financial challenges and economic fluctuations.

Conversely, SMEs that are not classed as ‘intensive’ and manage to break even stand to benefit significantly, potentially receiving relief rates nearly twice as high as the current rates.

Irrespective of policy shifts, adherence to compliance continues to be a crucial concern for both consultants and businesses self-administering their claims; in the financial year 2020-21, non-compliant claims led to losses exceeding £1 billion for the nation. Although no significant policy changes are anticipated in the short-to-medium term, it’s almost certain that the government will eventually introduce more stringent measures to combat fraud and non-compliance in the R&D tax credit sector.

Confused? That’s what we’re here for. Book a call with our team today.